With the MSCI World Crediting Strategy from Oceanview Life and Annuity Company, we continue our commitment to offering options designed to help today’s retiree or pre-retiree pursue growth opportunities while helping to protect principal, subject to product terms and limitations.

MSCI World FIA

Crediting Strategy

MSCI World FIA Crediting Strategy

In today’s interconnected economy, growth isn’t limited to a single country or sector. Companies operate globally, and opportunities can be found across developed markets around the world.

The MSCI World Index tracks large- and mid-cap companies across 23 developed countries, representing a broad cross-section of the global economy. With exposure to over 1,300 companies and approximately 85% of market capitalization in each country, the index is intended to represent the performance of developed equity markets worldwide.

A crediting strategy linked to the MSCI World Index offers interest crediting potential tied to global market performance—providing diversification beyond the U.S. while maintaining principal protection from market downturns. Amounts allocated to an index are not directly invested in the stock market or any index and do not include dividends. Index performance does not reflect actual investment results.

Contract Features of the Fixed Indexed

Annuity

- Premium Requirements

Minimum $20,000 - Issue Ages

3, 5-Year Up to Age 89 + 364 days

7, 10-Year Up to Age 84 + 364 days

(non-qualified and qualified assets) - Multi-Year Guaranteed Period Options

3, 5, 7, and 10 Years - Withdrawals

10% of Contract Value on or after first year of Contract anniversary without Surrender Change penalty.

Minimum Withdrawal Amount = $250 - Death Benefit

Account Value (No MVA or Surrender Charges) or Spousal continuation option - 20 Day Free Look period to cancel your contract

You may cancel the contract by sending it back to the issuing company. Upon cancellation, the company will return the purchase payment to you. Some states allow for 30 days Free Look. - Market Value Adjustment (MVA)

The MVA is a positive or negative adjustment based on the current interest rate environment at the time of withdrawal. An MVA and a surrender charge will apply if you access more than the 10% free withdrawal before the end of the initial interest rate guarantee period. The MVA does not apply to withdrawals after the surrender charge period, 10% free withdrawals, the death benefit, or when the contract is annuitized.*Please see your contract for additional details. Rider and calculations may vary by state.

Crediting Strategies of the Fixed Indexed

Annuity

The MSCI World Index crediting strategy may appeal to clients looking to complement US-focused strategies with broader global exposure –while maintaining the core benefits of a fixed indexed annuity. Don’t miss out on this opportunity – choose Oceanview Life for your retirement planning needs. This material is for informational purposes only and is not intended as investment, tax, or legal advice. Clients should consult with their financial professional regarding their individual situation.

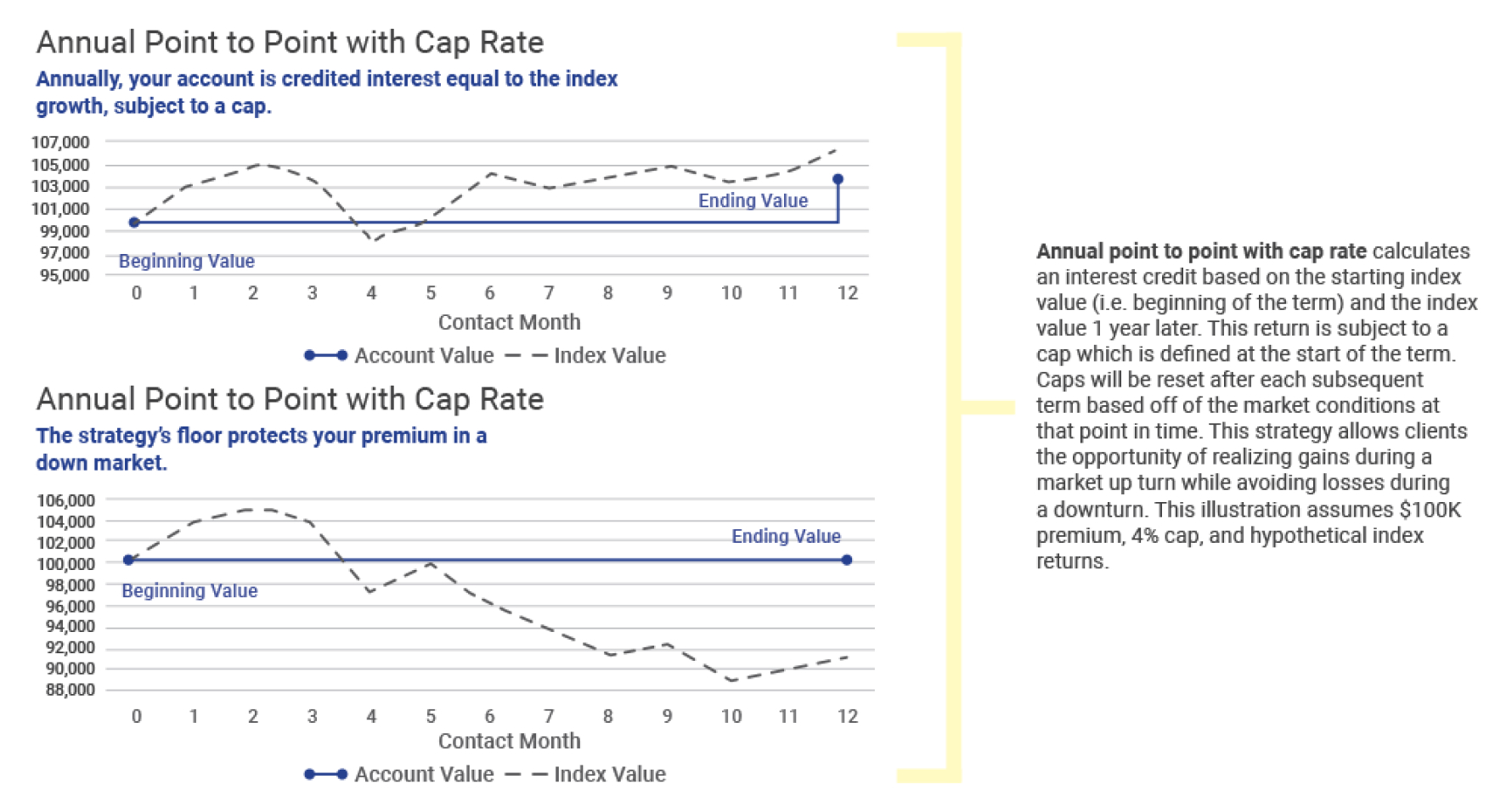

MSCI World Annual Point to Point with Cap Rate

Annual point to point with cap rate calculates an interest credit based on the starting index value (i.e. beginning of the term) and the index value 1 year later. This return is subject to a cap which is defined at the start of the term.

Riders of the Fixed Indexed Annuity

Nursing Home Confinement*: After the first contract anniversary, in the event that the contract owner is confined to a nursing home, any applicable MVA or surrender charges will be waived on any withdrawal. Nursing home confinement is defined as at least 90 consecutive days or at least 90 days if there is no more than a 6-month break in the confinement. Confinement must be prescribed by a qualified physician and medically necessary. Proof must be furnished to the Company during confinement or within 90 days after such confinement.

No Charge

Terminal Illness*: After the first contract anniversary, in the event that the contract owner is terminally ill and not expected to live more than 12 months, any applicable MVA and surrender charges will be waived on any withdrawal. Terminal illness must be diagnosed by a qualified physician after the contract’s issue date. Proof of terminal illness must be provided to the Company.

No Charge

*Waiver of surrender and MVA charges based on final review of claim.

Terms of the Fixed

Indexed Annuity

Spousal Continuation: This option allows one spouse to continue the other spouse’s contract as the new annuitant. In the event of the death of one spouse, contracts that are jointly owned by spouses or a single-owner contract with a sole spouse beneficiary allow the surviving spouse to assume all rights to the initial agreement. The surviving spouse will have the ability to elect to continue the contract, collect any remaining and all payments and any death benefits and choose beneficiaries, subject to certain conditions. This provision allows for the surviving spouse to maintain a tax-deferred status and secure long-term financial stability.

*For most states, Harbourview FIA Policy Form: ICC19OLASPDA. Product features, options, form numbers and availability may vary by state.This is a brief description of the Harbourview FIA and is meant for informational purposes only. It is not individualized to address any specific investment objective. It is not intended as investment or financial advice.

Settlement Options of the Fixed

Indexed Annuity

The Harbourview Fixed Indexed Annuity (FIA) can provide an income stream for a term of your choosing, including the rest of your life.

Life Only: Equal monthly payments for the annuitant’s remaining lifetime. Payments will end with the payment due just before the annuitant’s death.

Life with 10-Year Period Certain: Equal monthly payments for the greater of 120 months or the annuitant’s remaining lifetime.

Joint and Last Survivor: This option provides payments during the lifetime of the annuitant and the lifetime of a designated second person. If at the death of the survivor, annuity payments have been made for less than 120 monthly periods, the remaining guaranteed annuity payments will be continued to the beneficiary.

*Once annuity payments have begun, no changes can be made.

*For most states, Harbourview FIA Policy Form: ICC19OLASPDA. Product features, options, form numbers and availability may vary by state.This is a brief description of the Harbourview FIA and is meant for informational purposes only. It is not individualized to address any specific investment objective. It is not intended as investment or financial advice.

Download our Client Brochure

Why Choose a Fixed Index Annuity? Download our Pre-Retirement and Retirement Planning Tool to Learn More.