About LevelCap

Q: How does LevelCap differ from other Fixed Indexed Annuities (FIAs)?

Traditional FIAs generally reset their cap rates annually, creating uncertainty about future returns. LevelCap provides greater predictability by locking the cap rate declared at issue for the full surrender charge period. After the Surrender Charge Period, any funds in Guaranteed Cap Rate Strategies automatically transition to non-guaranteed cap strategies based on the current declared cap rates in effect at that time.

Q: What does it mean that the cap is “level”?

The cap rate is fixed and does not change throughout your chosen Surrender Charge Period (5 or 7 years). It provides stability and consistency for clients building long-term retirement strategies.

Q: When can a client allocate to a Guarantee Cap Rate Index Strategy?

The Cap Rate Guarantee Index Strategies are only available at the time of application. If a client elects to reallocate out of a Cap Rate Guarantee Fund to another fund, the client cannot reallocate back into any of the Guarantee Cap Rate Index Strategies.

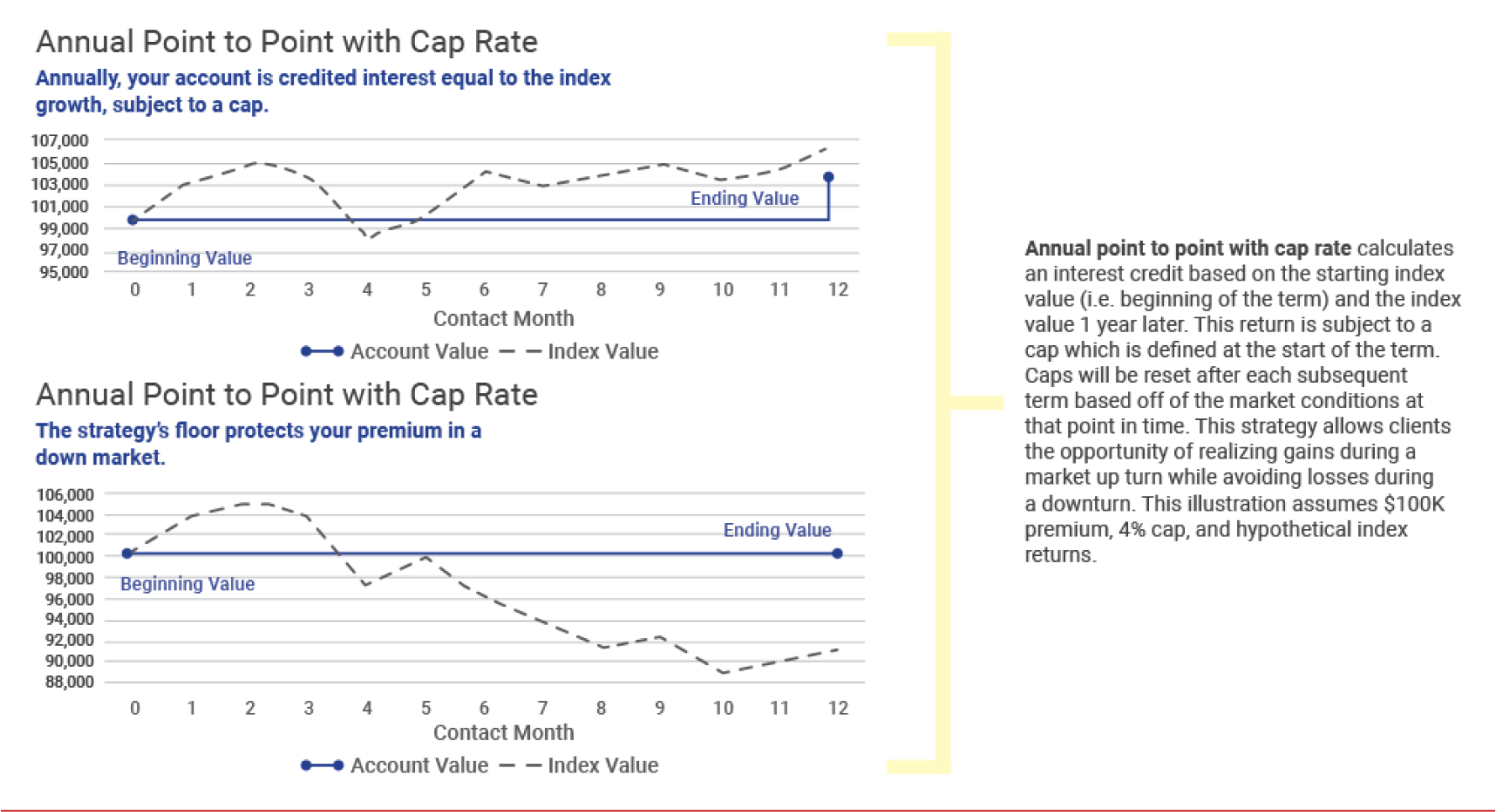

Q: Are returns guaranteed?

No. The cap rate is guaranteed to remain unchanged, but actual credited interest depends on index performance. If the index performs poorly, the credited interest for that period may be zero; however, your principal will not decline due to market performance.

Q: What happens at the end of the Surrender Charge Period?

At the end of the Surrender Charge Period, clients can reallocate among available crediting strategies, or fully withdraw their account value without surrender charges or MVA. If the contract continues beyond the Surrender Charge Period, funds in Guaranteed Cap Rate Strategies will transition to non-guaranteed strategies based on the rates declared at that time.

Q: Can allocations be changed during the Surrender Charge Period?

Yes. Allocations between the available strategies can be made annually.

The Cap Rate Guarantee Funds are only available at time of application. If a client elects to reallocate out of a Cap Rate Guarantee Fund to another fund, the client cannot reallocate back into any of the Guarantee Funds.

If the contract is maintained after the Surrender Charge Period, the client can reallocate to any non-guaranteed index strategies, If the client does not reallocate into other available Index Strategies, any funds in the Guaranteed Cap Funds will be placed into a non-guaranteed cap strategy subject to current declared cap rates.

About Fixed Indexed Annuities

Q: Is the money invested in the market?

No. The annuity does not directly invest in the stock market. Interest, if any, is credited based on index performance and subject to a cap or participation rate. The performance of the external index is used only as a reference to determine credited interest and does not reflect dividends or direct market participation.

Q: Can the contract lose value due to market declines?

No. Principal and previously credited interest are protected from market losses. All guarantees are backed by the claims-paying ability of Oceanview Life and Annuity Company.

Q: How is interest determined?

Interest is credited at the end of each crediting period, typically one year, based on the index’s performance and your selected crediting method. Interest crediting formulas vary by index strategy and are described in the contract.

Q: What are the liquidity options?

After the first contract year, up to 10% of the account value can be withdrawn annually without surrender charges or MVA. RMDs are also considered free withdrawals. Withdrawals may be subject to income tax and, if taken before age 59½, an additional 10% federal tax penalty.

Q: What is a Market Value Adjustment (MVA)?

(Not applicable in California.) The MVA adjusts the value of withdrawals beyond the free allowance based on interest rate changes. It may either increase or decrease surrender value. The MVA does not apply after the Surrender Charge Period and cannot reduce the value below the minimum guaranteed surrender value.

Q: What charges apply?

There are no explicit annual policy or administrative fees. Withdrawals exceeding 10% of account value during the Surrender Charge Period are subject to surrender charges and, if applicable, an MVA.

Q: Are any riders included?

Yes. Two built-in riders are provided at no cost:

- Nursing Home Confinement Waiver

- Terminal Illness Waiver

Availability and specific terms may vary by state. See contract for details.

Q: What happens upon the owner’s death?

Beneficiaries receive the full contract value, free from surrender charges and MVA. A spousal continuation option allows the surviving spouse to continue the contract.

Q: Is LevelCap available in all states?

LevelCap is available in most U.S. states but not currently offered in New York or Vermont. California versions are non-MVA.

About Oceanview

Q: Who backs the guarantees?

All guarantees are backed by the claims-paying ability of Oceanview Life and Annuity Company, rated A (Excellent) by A.M. Best and supported by Bayview Asset Management’s institutional investment expertise. A.M. Best rating as of December 11, 2024; ratings are subject to change and do not apply to the investment performance of any index.

Q: What are the tax advantages of an FIA?

FIAs grow tax-deferred, meaning taxes are only due when funds are withdrawn, allowing potential compounding over time.

Q: Who is LevelCap best suited for?

LevelCap may be appropriate for investors seeking:

- Principal protection from market losses

- Predictable cap rates over fixed terms

- Simplified, transparent accumulation strategies that complement broader portfolio planning

Product suitability should be determined based on the client’s financial situation, investment objectives, and time horizon. Clients should consult their financial professional to determine whether this product meets their needs and objectives.